WE'RE THE PEOPLE WHO PROVIDE STRATEGIC FINANCIAL PLANNING DESIGNED TO BRING YOUR AMBITIONS TO LIFE.

WHO ARE WE?

We’re Future Planners, a boutique financial planning business delivering strategic advice and hands on service across the financial planning spectrum. Between us we bring more than 100 years of financial planning experience to the business and, based on this, we’ve been building long term relationships with a growing and loyal group of clients who understand the value of our collective expertise and client centric approach to financial planning.

OUR APPROACH

People come to us with a wide range of needs. They may have an immediate financial query; they might have lost their way or hit a brick wall in personally managing their finances for one reason or another. They may just want our help in achieving their goals and their dreams. At Future Planners we devote ourselves to understanding these objectives and assisting our clients in reaching their goals and fulfilling their dreams.

LATEST NEWS

YOUR FINANCIAL FUTURE IS OUR BUSINESS

We have the expertise and experience to provide a comprehensive financial service for each and every client. Taking the time to understand your position and priorities, we tailor a strategic plan to meet your specific needs. Our strategies are based upon the understanding that clients need to plan for and build on those areas they can see and control, and as far as possible, protect against those they cannot.

ASSESSING RISK

GROUP CLIENT MEETINGS

INVESTMENT PHILOSOPHY

ONGOING REVIEWS

PROFESSIONAL PARTNERING

SELF MANAGED SUPER FUNDS

STRATEGIC FINANCIAL PLANNING

WEALTH ACCUMULATION

FUTURE PLANNERS FINANCIAL SERVICES SPECIALISES IN TAILORING FINANCIAL PLANNING SOLUTIONS FOR EACH INDIVIDUAL.

WE HELP YOU PLAN FOR THE REAL WORLD

CASE STUDY

"A family man, who after a 12 hour day paid little attention to where the money was going, so bills and credit card debt kept mounting even though the business is flourishing and new work is plentiful."

READ MORE

OUR CLIENT

A hard working tradesman operating a family run business with little time or expertise in maximising the fruits of his hard labour. A family man, who after a 12 hour day paid little attention to where the money was going, so bills and credit card debt kept mounting even though the business is flourishing and new work is plentiful. His sub-contractors are on a good wicket as he pays them weekly on time and in full, including super. The clients already had a self-managed superannuation fund with only $12,000 in it – yes $12,000, costing 20% per annum for compliance and administration. In addition, he had a small fund balance in an industry fund with minimal life insurance, outstanding tax liabilities and debt on their home, rental property and credit card. He had cash but it was locked in the business, outstanding invoices and was time poor. With a very busy and successful year and no planning for the current tax liability, some quick action was required. What the clients needed was some direction and guidance, a plan and regular reviews with someone who can get the job done leaving the tradesman to do what he does best.

THE ISSUE

- What to do with the SMSF

- How to reduce credit card debt

- Family protection in case of death or disability

- Tax liabilities

THE SOLUTION

By refinancing their home and rental property, sufficient equity was created to pay all the credit card debt and outstanding tax. Ongoing interest costs are now reduced.

With assistance from one of our preferred accountants, we restructured the business, added a corporate beneficiary to the family trust, established an accounting package to control and collect outstanding debts and more importantly, allowed for monthly profit and loss reports to be generated.

We then formulated a strict personal budget, commenced paying weekly salaries exactly the same as the sub-contractors and paid Pay As You Go Tax.

The SMSF was a real problem, but in the interim we contributed maximum contributions of $35,000 each from the business account, thereby reducing company tax liabilities and arranged for the self managed super fund to purchase life insurance on the tradesman and his wife. Income protection was taken out personally as these premiums attract a full personal tax deduction. The industry super account balance was rolled into the SMSF. With a larger balance now in their self managed fund, compliance and administration costs become more realistic and although still too high, will reduce in proportion to the size of the fund over time. The contributions also allowed for an appropriate investment strategy to be implemented.

We addressed their estate planning, death benefit nominations and asset protection arrangements.

Now the client has peace of mind knowing his hard labour is worthwhile and his retirement planning is on track. Both he and his wife have someone to whom they can refer if they have financial questions or concerns and a relationship with a business that will assist them with an annual review to help them keep on track.

CASE STUDY

"They had an existing SMSF holding a mish mash of underperforming investments valued at about $250,000. They sought advice because they felt their personal retirement plans had no direction and lacked impetus."

READ MORE

OUR CLIENT

A couple who attended one of our Retirement Planning seminars decided to follow up to do a full review of their personal and financial circumstances. In their early 50’s, both working and a child still living with them, they had a home worth around $1 million and no mortgage. She had salary of $80,000 and he had a small business turning over $150,000 a year. They had an existing SMSF holding a mish mash of underperforming investments valued at about $250,000. They sought advice because they felt their personal retirement plans had no direction and lacked impetus.

THE ISSUE

Their focus in the past had been on paying off the house and educating their children. They had not been contributing more than the legislated amount to super and from the business revenue of $150,000 a year, operating expenses were $54,000 including $2,000 a month on rent. If they kept going down this path, they could not see how they could afford to retire.

THE SOLUTION

The first step was to understand what income they needed to live comfortably and a detailed budget was prepared with them. Once that was known, we were able to:

- Commence a salary sacrifice regime of $8,000 pa for her, taking her taxable income down to $72,000, saving $2,720 in personal tax

- Reduced the income he drew from the business from $96,000 to $50,000 a year saving $16,360 in personal tax

- Used $25,000 of the savings to contribute to super as tax deductible contributions

- Recommended he purchase a business premises in their existing SMSF using the SMSF borrowing rules, the $21,000 remaining savings from business income and the $24,000 rental savings

- Facilitated an appropriate loan arrangement

- Increased annual concessional contributions from $7,200 to $40,000

- Added a $500,000 building to the SMSF and $45,000 a year from rental and redirected business income

CASE STUDY

"Their ability to meet the RAD payments was going to be extremely tight, both in the short and long term and the family had no idea how they were going to do it."

READ MORE

OUR CLIENT

Mr and Mrs L had been living in a retirement village. All was going well until Mr L’s failing health meant that he began to rely on his wife more and more for help with his normal daily care needs. As a result, Mrs L’s health also started to deteriorate and they were both eventually admitted to an Aged Care facility for a period of respite. It was hoped this would provide an opportunity for both to recuperate and return home, but Mrs L enjoyed herself so much in the facility, she decided she didn’t want to leave. She felt liberated from the constant needs of her beloved and the daily grind of keeping their lives running. The situation was discussed with the management of the Aged Care facility who provided the family with a price for two permanent places and a time limit to get things sorted out.

The family were desperate for help.

THE ISSUE

Money was a problem. Whilst the cost of placement was fair, the couple’s assets did not cover two full placement fees (Refundable Accommodation Deposits or RAD) of $400,000 each.

Their unit in the retirement village would need to be sold and they were told that there was some buyer interest, but sale of retirement village units can be a long slow process. Moreover, whilst valued at $710,000, 30% of the sale price was to be retained by the village. In addition, 3% commission was payable to the village for the sale of the unit and a further $15,000 to $20,000 would be charged for refurbishment in preparation for the next owner. This meant that Mr and Mrs L would receive around $460,000 from the sale price of $710,000 – a cost of $250,000. They had around $50,000 in other saleable assets and that was it. Their ability to meet the RAD payments was going to be extremely tight, both in the short and long term and the family had no idea how they were going to do it.

The paperwork necessary for government assessment of Mr and Mrs L’s financial position had not been completed. This meant that the Aged Care facility could not get the placement or the fees finalised. However, we saw that it also provided us an opportunity to have the couple assessed as ‘low means’, resulting in a saving on the Refundable Accommodation Deposits of nearly $200,000 each.

They had a tight time limit.

This time in a family’s life is usually stressful and highly emotional and this was certainly how we found Mr and Mrs L’s children and grandchildren. The family were stressed and did not know where to start to get things sorted out and their parents/grandparents safely and happily placed in the Aged Care facility of their choice. No one in the family had spare money to assist, even in the short term.

THE SOLUTION

Initially we met with the family representative to discuss the situation in detail and by the end of that first meeting we were able to provide them with an interim plan of action just to keep things going financially until a longer term plan could be devised. We agreed that the long term plan would be presented in a Statement of Advice.

The advice document was written within a week and it outlined in detail, the options that were available and the steps the family needed to take to meet the tight time limit. It also directed them as to the best approach to take to minimise the fees payable to the Aged Care facility and to improve their parents’ ongoing cash flow. It provided both capital and cash flow outcomes of each of their options. It took a situation that had at first appeared almost out of their reach over the longer term, to one that gave them plenty of room to move. It also provided the whole family support and a clear path forward. We met with the family again to go through the advice to ensure they understood the options and recommendations made. It was quite a relief for them to see that it could be done.

With their decisions made, we provided direction with completion of the relevant government and Aged Care paperwork and assisted with the liquidation of the parents’ investments so debts could be paid and ongoing costs of living could be met.

As a result of our work, a reduced Refundable Accommodation Deposit of $206,000 each was achieved, all necessary paperwork was completed correctly and Mr and Mrs L now have permanent placement in the facility of their choice. It was a great outcome for the whole family.

CASE STUDY

"She created a SMSF and added the remaining $150,000, rolled over her employer super fund balance and without a mortgage, managed to salary sacrifice to the maximum."

READ MORE

OUR CLIENT

A single female in her late 40’s living in a small first floor apartment in Melbourne CBD. Property valued at $500,000 with a mortgage of $200,000. A salary of $100,000 and an employer superannuation plan of $150,000 sought advice because she needed direction and did not know what to do.

THE ISSUE

Apart from her own financial issues, a major concern for her was her mother who was 84 and lived alone in the big family home in Sydney. Her mum was finding it increasingly difficult to maintain the house, but did not want to contemplate Aged Care. As an only child, it was up to our client to look after the welfare of her mother who had no other assets apart from the family home (worth $1.2M) and survived on the full Age Pension. They discussed the option of mum moving to Melbourne, but she was very concerned about the impact this would have on her pension.

Our client knew that if her mother moved to Melbourne, they could not both live in her existing apartment and if she sold that, she would only have $300,000. They were very keen to buy a ground floor apartment they had seen for $1.2M and asked for our advice.

THE SOLUTION

- Sell the Sydney property (with appropriate Real Estate advise)

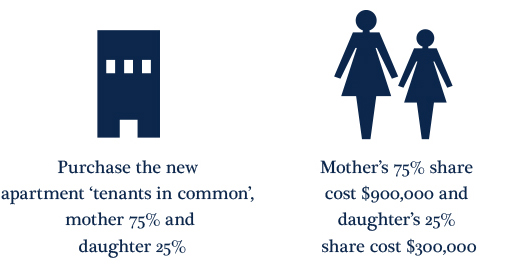

- Purchase the new apartment ‘tenants in common’, mother 75% and daughter 25%

- Mother’s 75% share cost $900,000 and daughter’s 25% share cost $300,000

- Under Centrelink rules, mother could ‘gift’ $150,000 to daughter under the ‘Granny Flat Interest’ rule without affecting her Age Pension entitlement

- Mother was left with $150,000 in the bank and very close to the full Age Pension and on her passing, her share of the property would pass to her daughter via her Will

- Daughter was able to use the Granny Flat Interest amount of $150,000 and $150,000 of her own money to purchase her share of the property with no mortgage

- She was on hand to support her mother

- She created a SMSF and added the remaining $150,000 from the sale of her apartment, rolled over her employer super fund balance and without a mortgage, managed to salary sacrifice to the maximum